Africa is one of the most dynamic regions in the global payments landscape, driven by rapid mobile adoption, real-time payment infrastructure, and a strong push toward financial inclusion. As digital commerce expands and consumers increasingly embrace electronic transactions, understanding local payment methods has become essential for banks, fintechs, and merchants operating across the continent.

With Africa’s e-payments market revenues expected to grow by approximately 20% annually reaching around USD 40 billion by 2025, the region presents significant opportunities alongside operational complexity. Each market has distinct rails, regulatory frameworks, and consumer preferences, from Nigeria’s real-time transfer ecosystem to Ghana’s mobile money dominance and Egypt’s national payment networks.

For organisations expanding into Africa, success depends on the ability to support local payment methods, optimise acceptance rates, and manage multiple integrations efficiently. In this guide, we explore the most widely used payment methods in Nigeria, South Africa, Ghana, and Egypt, alongside the trends shaping the continent’s evolving digital payments ecosystem and how Paysecure is support global merchants to successfully localise their offering for this market.

Overview of Africa’s digital payment landscape

Africa’s payments growth is underpinned by powerful demographic and technological trends. The continent has the fastest population growth rate globally at approximately 2.7% annually and a median age of around 20 years, creating a digitally native consumer base that is highly receptive to mobile-first financial services.

Mobile money continues to play a central role. Globally, registered mobile accounts reached 1.75 billion in 2023, with 856 million located in Africa alone. Transaction volumes exceeded 62 billion, highlighting the scale of mobile-led financial activity across the region.

Interoperability initiatives such as national QR schemes, including Ghana’s GHQR and Nigeria’s NQR, are enabling seamless transactions across bank accounts, cards, and mobile wallets. At the same time, real-time payment infrastructure is expanding rapidly, with several African markets ranking among global leaders for instant transactions.

Regulatory developments, including open banking frameworks and tiered KYC models, are further accelerating innovation by enabling new business models and reducing barriers to entry for fintech providers.

For banks and merchants, these developments unlock opportunities to:

- Capture growing digital commerce volumes

- Deliver embedded financial services

- Expand into underserved customer segments

- Launch payments-as-a-service capabilities

- Build integrated financial ecosystems across channels

“To stay competitive in the global digital transformation trend, Africa must reduce friction in both domestic and cross-border payments. With Paysecure’s whitelabel solution, banks and businesses alike can deploy their own branded payment gateway, underpinned by dedicated servers and PCI DSS-compliant software. Our setup guarantees robust security measures and a user-friendly interface that meets the diverse needs of both consumers and businesses.”

Payment methods in Nigeria: A leader in real-time payments innovation

Nigeria has emerged as one of Africa’s most advanced digital payments markets, driven by strong fintech innovation, regulatory support, and widespread adoption of instant transfers.

- Instant payments: Nigeria Inter-Bank Settlement System

- The Instant Payment (NIP) system, operated by the Nigeria Inter-Bank Settlement System Plc (NIBSS), is the largest instant payment scheme in Africa and among the top globally. Supporting real-time transfers across dozens of banks and financial institutions, NIP processed electronic transactions worth approximately N387 trillion in 2022. Its availability across mobile apps, internet banking, USSD, ATMs, and POS channels has made instant transfers a foundational payment method for both consumers and businesses.

- Open banking

- Nigeria has standardized API access to Open Banking solutions, allowing for seamless integration and fostering innovation. NIBSS plays a crucial role in supporting government-to-person (G2P) payments, hosting and validating transactions for all governmental social intervention programs.

- Mobile payments and USSD

- Mobile payment platforms such as Paga and OPay have driven significant growth in digital transactions, supported by increasing smartphone penetration. USSD remains critical in areas with limited internet connectivity, enabling accessible financial services through simple mobile interactions.

- Card payments

- Debit and credit cards, primarily issued through global networks like Visa and Mastercard, remain widely used for both online and in-store transactions. Growing merchant acceptance continues to support card usage across sectors.

- Bank transfers and online gateways

- Direct bank transfers are popular due to their convenience and perceived security, particularly for higher-value transactions. Payment gateways facilitate eCommerce growth by streamlining checkout experiences.

- QR payments

- NQR – Nigeria’s New Quick Response (NQR) platform enables interoperable QR payments across banks and wallets, supporting contactless transactions and expanding digital acceptance.

- Digital banks and wallets

- Digital banking platforms such as Kuda are gaining traction by offering mobile-first financial services that improve accessibility and user experience.

For businesses operating in Nigeria, supporting instant transfers alongside mobile and card payments is essential to maximise conversion and customer reach.

Payment methods in South Africa: Mature infrastructure meets digital innovation

South Africa combines well-established banking infrastructure with growing adoption of alternative payment methods, making it one of the continent’s most sophisticated payment environments.

- Card payments dominance

- Debit cards remain the most commonly used online payment method, accounting for approximately 58% of transactions. Credit cards also maintain strong adoption due to consumer familiarity and built-in protections.

- Real-time payments growth

- The real-time payments market, valued at USD 11.44 billion in 2021, is projected to reach nearly USD 25.90 billion by 2026, reflecting strong demand for faster settlement and digital convenience.

- Bank transfers (EFT)

- Electronic Funds Transfer remains widely used, particularly for bill payments and large transactions, offering consumers direct control over funds movement.

- Digital wallets

- Mobile wallet solutions such as SnapScan and Zapper enable quick, contactless payments and are increasingly popular across retail and hospitality environments.

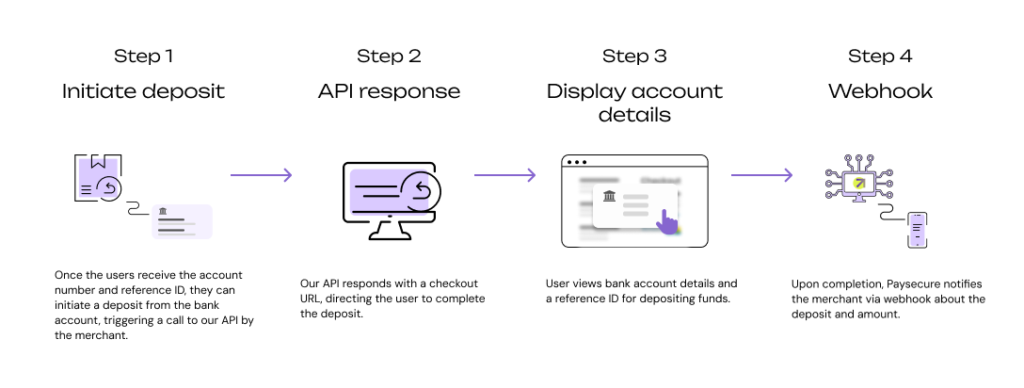

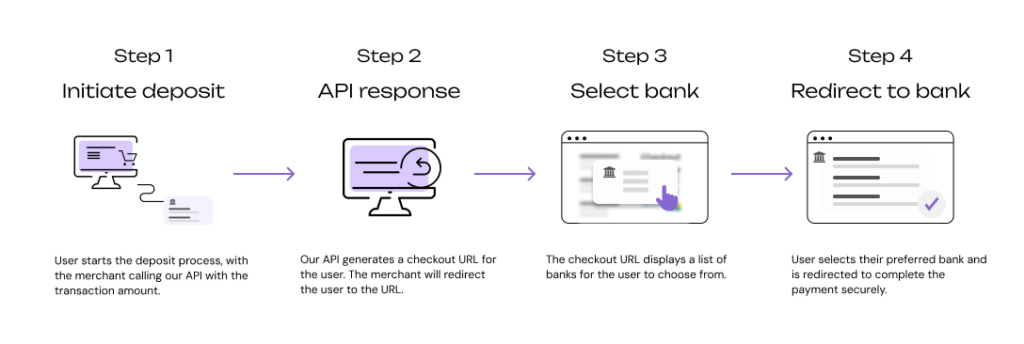

South Africa’s blend of traditional and digital payment methods requires flexible infrastructure capable of supporting multiple rails simultaneously. At Paysecure we offer intuitive payment flows through our comprehensive orchestration platform. This simplifies the transaction process for end-users. Whether it’s through Account Transfers (Manual EFT) or Instant EFT, our platform ensures seamless interactions that enhance user satisfaction and increase transaction completion rates. Here is how simple and efficient our flow is:

Account transfer (Manual EFT):

Instant EFT:

Payment methods in Ghana: Mobile money at the core of financial activity

Ghana has built one of the most vibrant mobile money ecosystems globally, supported by strong regulatory frameworks and widespread consumer adoption.

- Mobile money leadership

- Mobile money platforms dominate everyday transactions. In 2023, transaction values reached approximately GH¢1.912 trillion, an 82% increase year-on-year demonstrating the scale of digital financial activity. Monthly transaction volumes regularly exceed GH¢100 billion, while long-term projections suggest continued growth across the sector.

- Digital wallets and payment platforms

- Solutions such as GTPay, ExpressPay, Interpay, and Myghpay support online payments and contribute to a diverse digital ecosystem.

- GHQR national QR scheme

- GHQR enables instant payments across banks and mobile wallets, improving interoperability and reducing friction for both merchants and consumers.

- Blockchain experimentation

- Emerging use cases leveraging blockchain technology are enabling faster and lower-cost transfers while improving transparency across financial systems.

- Cross-border wallets

- Solutions like the USD Global Wallet facilitate international transfers, supporting trade and financial connectivity.

Ghana’s payments environment highlights the importance of supporting mobile-first experiences alongside interoperable infrastructure.

Payment methods in Egypt: National schemes driving digital adoption

Egypt’s payments landscape is shaped by government initiatives and national infrastructure designed to expand electronic payments and financial inclusion.

- National payment networks

- Systems such as Meeza Digital and InstaPay provide foundational infrastructure for electronic transactions, supporting both consumer and merchant use cases.

- Mobile wallets

- Services including Vodafone Cash and Orange Money enable convenient digital payments and continue to grow in popularity.

- Card usage

- Debit and credit cards remain widely used, supported by strong banking penetration and expanding eCommerce activity.

- Payment networks like Fawry

- Fawry plays a central role by enabling bill payments, cash-in services, and online transactions across a vast network of physical and digital channels.

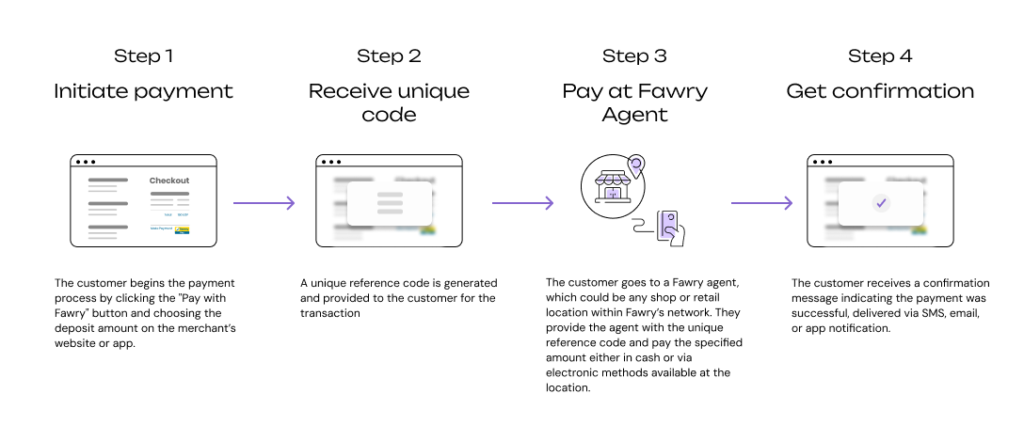

Egypt’s evolving ecosystem reflects a broader shift toward integrated payment solutions across both digital and physical environments. In Egypt, our solution empowers consumers to utilise Fawry Pay for fund transfers from their bank accounts or through Fawry’s extensive network of retail locations and online services. Fawry is a leading Egyptian payment network that facilitates secure transactions both online and offline across a variety of financial services. This platform provides multiple payment options, including Fawry Pay.

Paysecure’s Fawry PayIn feature leverages this robust payment network to support diverse collection scenarios. Merchants can initiate payment requests via mobile apps, online platforms, or physical retail points, offering secure, efficient, and flexible options for collecting payment from customers.

Paysecure’s Fawry flow:

Managing complexity across Africa’s fragmented payment ecosystem

While Africa presents significant growth opportunities, operating across multiple markets introduces complexity. Payment methods vary widely by country, and businesses must navigate different regulatory requirements, settlement processes, and consumer expectations.

Key challenges include:

- Integrating multiple local payment providers

- Managing cross-border transactions and currencies

- Optimising approval rates across different rails

- Ensuring compliance with local regulations

Maintaining visibility across payment performance

A unified payment orchestration platform, such as Paysecure, addresses these challenges by enabling businesses to connect to multiple providers through a single integration, apply intelligent routing logic, and gain real-time insights into transaction behaviour.

Enabling growth with orchestration and local payment expertise

Payment orchestration plays a critical role in helping businesses succeed across Africa’s diverse and rapidly evolving payments landscape. By supporting local payment methods and connecting to regional payment rails through a unified orchestration layer, businesses can build trust, improve conversion, and deliver payment experiences that feel relevant to customers in each market.

With intelligent routing, granular performance data, and real-time visibility, merchants can continuously optimise how payments are processed; understanding which providers, methods, or flows perform best by country, customer segment, or channel. Customer segmentation capabilities enable tailored payment journeys, dynamic rules, and more personalised experiences that reduce friction and support stronger engagement and lifetime value.

Comprehensive payment platforms, like Paysecure’s orchestration solution, are designed for complex payment environments and enable organisations to:

- Expand into new markets faster through a single integration layer connecting local and global payment methods

- Improve acceptance rates with intelligent routing across providers and payment rails

- Reduce operational overhead by simplifying integrations and operational complexity

- Leverage granular reporting to monitor approval rates, payment performance, and regional trends

- Apply customer segmentation to optimise checkout flows and tailor experiences to different audiences

- Gain actionable insights to refine payment strategies and improve customer outcomes

- Ensure consistent compliance and operational resilience across regions

By combining local payment expertise with orchestration, data intelligence, and optimisation capabilities, businesses can move beyond simply accepting payments to delivering seamless, high-performing experiences across African markets.

Unlocking opportunity in Africa’s fast-growing payments landscape

Africa’s digital payments ecosystem continues to evolve rapidly, driven by mobile innovation, real-time infrastructure, and increasing demand for seamless financial services. From Nigeria’s instant transfer leadership to Ghana’s mobile money dominance and Egypt’s national payment networks, each market presents unique opportunities for growth.

For banks, fintechs, and merchants, success depends on understanding local payment preferences and deploying infrastructure that can adapt to diverse environments. By supporting the right payment methods and leveraging tools such as Paysecure’s orchestration platform to manage complexity, you can capture the full potential of Africa’s expanding digital economy.

For more information on how Paysecure can support you in Africa and beyond, get in touch with the team today.